If you have started thinking seriously about your retirement, chances are you have already typed “Best SIP to Invest Now” into Google at least once. It is a fair question. With pension coverage still limited in India and joint family support systems weakening in cities, most of us are on our own when it comes to building a retirement corpus.

A Systematic Investment Plan, or SIP, has become the preferred route for salaried professionals and self employed individuals alike because it turns retirement saving into a monthly habit rather than a once a year scramble.

This article is written to help you understand how to identify the best SIP to invest now for your own retirement goal, what factors actually matter, and which mistakes to avoid.

There is no single fund that is universally “best” for everyone, because your age, income, risk appetite and years left to retirement are different from your neighbour’s. What we can do is give you a framework that works, backed by real numbers and real examples.

Why SIP Has Become the Default Choice for Retirement Planning in India

Ten years ago, most Indian households parked retirement savings in Fixed Deposits, PPF and LIC policies. That is changing fast. Retail investors have realised that equity linked SIPs, held over long periods, tend to beat inflation by a wider margin than traditional instruments.

The scale of this shift is visible in AMFI’s own numbers. According to the Association of Mutual Funds in India monthly data, SIP contributions touched a record high of around Rs 32,087 crore in March 2026, and SIP assets under management crossed Rs 17 lakh crore, now accounting for nearly one fifth of the entire mutual fund industry’s AUM.

That is not a small trend limited to metro cities anymore, it is a nationwide shift in how Indians are choosing to build wealth for the long term, including retirement.

The second number worth noting comes from industry reporting on the same AMFI dataset, which showed the total mutual fund folio count growing from around 70 lakh in 2016 to over 27.6 crore by May 2026, a roughly 35 fold jump in a decade (source: StartupTalky, AMFI data analysis).

This tells you something important: SIP investing has moved from a niche practice among finance savvy investors to a mainstream habit across income groups. If you have not started yet, you are actually a bit behind the curve, not ahead of it.

Related: Is SIP Good or Bad for Long-Term Wealth Creation?

What Actually Makes a SIP “Best” for Retirement

Before picking a fund, it helps to separate two very different questions that people often mix up. One is “which fund category suits my goal”, and the other is “which specific scheme should I pick”. Getting the first one right matters far more than the second, because category and asset allocation drive the bulk of your long term returns, while individual scheme selection only fine tunes the outcome at the margin.

1. Match the SIP to Your Time Horizon

Retirement planning is a long game, usually spanning fifteen, twenty or even thirty years depending on your current age. The general rule that financial planners in India follow is simple: the longer your horizon, the higher the equity allocation you can afford to carry, because you have time to ride out market corrections.

- 25 to 35 years of age, 25+ years to retirement: A higher allocation to Flexi Cap, Mid Cap and even a portion in Small Cap funds is workable, since short term volatility has time to smooth out.

- 36 to 50 years of age, 10 to 24 years to retirement: A more balanced mix of Large Cap, Flexi Cap and Hybrid funds tends to work better, reducing dependence on any single market segment.

- 50 years and above, under 10 years to retirement: This is the phase to start shifting a growing portion into Hybrid, Balanced Advantage and Debt oriented funds to protect the corpus you have already built.

2. Check the Expense Ratio and Fund House Track Record

A fund’s expense ratio might look like a tiny percentage, but over a twenty year SIP it compounds into a meaningful difference in your final corpus. Direct plans, where you invest without a distributor, typically carry a lower expense ratio than Regular plans for the same scheme.

Many long term investors in India now prefer Direct plans through platforms like the AMC website, Groww, Zerodha Coin or Kuvera, precisely for this reason.

Fund house track record matters too, not because past returns guarantee future ones, but because a house that has managed money through multiple market cycles, including 2008, 2020 and the recent volatility of 2025 to 2026, tends to have more disciplined risk management processes in place.

3. Look at Consistency, Not Just Recent Returns

A fund that shot up 40 percent in one calendar year but fell harder than its peers during a correction is not necessarily a safer bet for retirement money. What you want is a scheme that has stayed in the top half of its category across multiple three year and five year rolling periods, rather than one that had a single spectacular year followed by underperformance.

SIP Categories to Consider for Retirement Goals

| Fund Category | Suitable Investor Profile | Typical Role in Retirement Portfolio |

|---|---|---|

| Flexi Cap / Multi Cap | Most investors across age groups | Core holding, diversifies across company sizes automatically |

| Large Cap | Conservative investors, those closer to retirement | Stability, lower volatility compared to mid and small cap |

| Mid Cap and Small Cap | Younger investors with long horizon and high risk tolerance | Growth booster, higher potential but higher swings too |

| Hybrid / Balanced Advantage | Investors within 5 to 10 years of retirement | Cushions volatility while still participating in equity upside |

| ELSS (Tax Saver) | Salaried investors seeking Section 80C benefit | Dual purpose, tax saving plus long term equity growth, three year lock in per instalment |

| Debt / Retirement Oriented Funds | Near retirement or already retired | Capital protection, regular income planning |

A Real World Example: How a Monthly SIP Can Build a Retirement Corpus

Let us take a realistic example instead of a hypothetical one. Consider a 30 year old marketing professional based in Bangalore, earning a decent salary and starting a monthly SIP of Rs 10,000 with a plan to retire at 60. That gives thirty years of investing.

Assuming an illustrative average annual return of 12 percent, which is a reasonable long term assumption for a well diversified equity portfolio in India and not a guaranteed figure, the numbers work out roughly like this:

- Total amount invested over 30 years: Rs 36 lakh

- Approximate corpus at retirement: Rs 3.5 crore or more, depending on actual market performance

Now compare this with someone who starts the same SIP amount ten years later, at age 40, with only twenty years left to retirement. Even though they invest the same monthly amount, their total corpus could end up less than half, purely because they lost a decade of compounding.

This is the single biggest reason financial advisors in India keep repeating one line: start your SIP today, not next year, because time in the market matters more than timing the market.

Please treat this example as illustrative only. Actual returns depend on market conditions, fund selection and expense ratios, and mutual fund investments are subject to market risk.

SIP vs Lump Sum for Retirement Corpus Building

Many first time investors in India ask whether they should invest a lump sum bonus or annual increment instead of spreading it through SIP. For retirement planning specifically, SIP tends to be the more practical choice for most salaried individuals for a few reasons.

- It matches your income pattern, since most of us earn monthly, not in one large sum.

- It applies rupee cost averaging, buying more units when markets fall and fewer when they rise, which reduces the risk of investing everything at a market peak.

- It builds discipline through automation, since the amount gets debited before you get a chance to spend it elsewhere.

That said, if you do receive a bonus or matured FD, there is nothing wrong with topping up your retirement corpus through a lump sum in a Large Cap or Hybrid fund, as long as your core retirement savings continue through SIP.

Common Mistakes Indian Investors Make While Choosing a SIP for Retirement

Stopping the SIP During Market Corrections

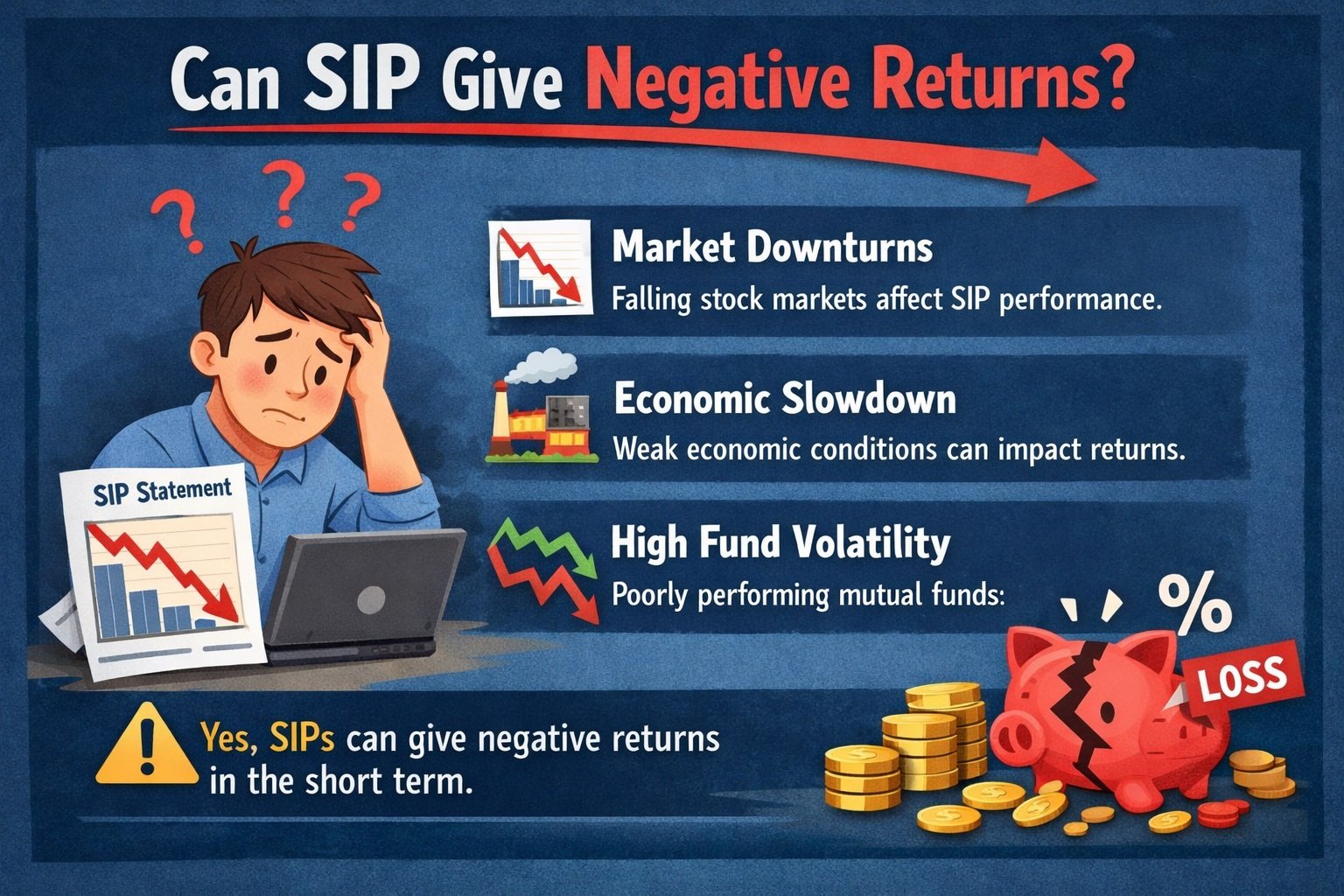

This is possibly the most damaging habit. AMFI’s own data has flagged rising SIP stoppage ratios during volatile months in 2026, meaning many investors are pausing or cancelling SIPs exactly when unit prices are lower and future returns are likely to be better. Retirement is a decades long goal, and pausing contributions during a temporary dip usually hurts the final corpus far more than it protects it.

Chasing Last Year’s Top Performing Fund

A fund that topped the charts last year rarely repeats that exact position the following year. Selecting a fund purely because it appeared at the top of a “best returns” list, without checking consistency across cycles, often leads to disappointment.

Ignoring Asset Allocation as You Age

Many investors set up a SIP in their late twenties and never revisit the fund category mix again. As retirement gets closer, shifting a portion of the corpus from pure equity to hybrid or debt oriented funds protects the wealth you have already accumulated from a sudden market downturn just before you need the money.

Not Increasing SIP Amount with Salary Growth

A Rs 5,000 SIP started at age 25 and never increased will not keep pace with rising living costs over thirty years.

Most financial planners recommend a step up SIP, increasing your monthly contribution by 10 percent every year in line with typical salary increments, which can significantly boost the final corpus without feeling like a heavy burden month to month.

Best SIP to Invest Now: 5 Schemes Across Different Retirement Needs

Once you have decided which category suits your age and risk profile, the next step is looking at actual schemes within that category. Below are five funds that are frequently discussed among Indian investors right now, each representing a different piece of the retirement puzzle rather than a one size fits all pick. Go through what each one actually does before deciding if it fits your own portfolio.

1. HSBC Multicap Fund

This is an equity scheme that invests across large cap, mid cap and small cap stocks, with a mandate to keep at least 25 percent of assets in each of the three segments at all times. That structure gives it built in diversification, since the fund manager cannot overload the portfolio into just one market cap category even during a rally.

For a retirement SIP, a multicap fund like this works well as a core holding for investors who want broad market exposure through a single scheme rather than juggling separate large cap, mid cap and small cap funds. It carries the higher volatility typical of mid and small cap exposure, so it suits investors with at least a ten year runway to retirement.

📈👉 Click Here for More Details.

2. HSBC Value Fund

This scheme follows a value investing style, meaning the fund managers look for companies trading below what they believe is their fair worth, rather than chasing the most popular sectors of the moment.

Value funds tend to go through phases where they lag growth oriented peers, followed by periods where they outperform once the broader market re rates those undervalued businesses.

For retirement planning, adding a value fund alongside a growth or multicap fund gives your portfolio a different return pattern, which can smoothen overall volatility across market cycles spanning many years.

📈👉 Click Here for More Details.

3. DSP Multi Asset Allocation Fund

Unlike pure equity funds, this scheme spreads money across equity, debt and commodities such as gold and silver, with each asset class typically maintaining a meaningful minimum allocation.

The logic here is straightforward: equity, debt and gold rarely move in the same direction at the same time, so combining them in one fund cushions the portfolio when equity markets turn volatile.

This category suits investors who want a single SIP that automatically rebalances across asset classes, and it becomes particularly relevant as you move within ten years of retirement and want to reduce dependence on equity alone.

📈👉 Click Here for More Details

4. Bandhan Small Cap Fund

This fund invests at least 65 percent of its assets in small cap companies, following what the fund house describes as a growth at reasonable price approach, meaning it looks for growing businesses without overpaying for them, while also keeping individual stock concentration in check.

Small cap funds carry the highest volatility among equity categories and can see sharp drawdowns during market corrections.

They are best suited to investors in their twenties or early thirties who have a genuinely long horizon, twenty years or more, and the temperament to stay invested through rough patches rather than a fund for someone nearing retirement.

📈👉 Click Here for More Details

5. Mirae Asset Gold Silver Passive FOF

This is a fund of funds that invests in gold and silver ETFs, aiming to track the combined price movement of both metals rather than picking stocks. Gold and silver have traditionally acted as a hedge during periods of equity market stress, currency depreciation or global uncertainty.

For a retirement portfolio, a small allocation to a gold and silver fund, typically in the range of 5 to 10 percent, can add a layer of protection that pure equity or debt funds do not provide. It should be treated as a diversifier within your overall SIP mix, not as the primary vehicle for building your retirement corpus.

📈👉 Click Here for More Details.

Fund categories and features mentioned above are based on publicly available scheme information and are provided for educational understanding only. This is not a recommendation to buy or sell any specific mutual fund scheme. Past performance of any fund does not guarantee future returns, and mutual fund investments are subject to market risk. Please check the latest factsheet, expense ratio, exit load and risk rating on the AMC website, and consult a SEBI registered investment adviser to see which of these, if any, genuinely fits your retirement goal, risk appetite and time horizon before investing.

How to Start Your Retirement SIP Today

- Complete your KYC through any AMC website, registrar portal like CAMS or KFintech, or a mutual fund investing app.

- Decide your monthly amount based on what you can commit consistently, not the maximum you can technically afford right now.

- Choose Direct plans over Regular plans if you are comfortable researching funds yourself, to save on the expense ratio over the long run.

- Split your SIP across two or three categories based on your age and risk profile, rather than putting everything into one fund.

- Set up an auto debit mandate so the investment happens on the same date every month, without you needing to remember.

- Review your portfolio once a year, not every week, and rebalance only when your goals or risk profile genuinely change.

Frequently Asked Questions

What is the best SIP amount to start for retirement planning?

There is no fixed number that works for everyone. A commonly used guideline is to direct at least 15 to 20 percent of your monthly take home income toward retirement focused SIPs, and to increase this percentage as your income grows.

Can I change my SIP fund later if it underperforms?

Yes, you can switch between schemes, though it is worth checking the exit load and tax implications first. It is better to review performance over a three year window rather than reacting to short term underperformance.

Is ELSS a good option for retirement SIP?

ELSS works well for investors who also want to claim Section 80C tax deduction, since it combines equity growth with tax savings. However, since each instalment carries its own three year lock in, it works best as one part of your retirement portfolio rather than the only fund you rely on.

How much corpus do I actually need for retirement in India?

This depends heavily on your expected monthly expenses after retirement, inflation, and how many years you expect to live post retirement. A commonly used starting point is to target a corpus that is 25 to 30 times your expected annual expenses at the time of retirement, though a certified financial planner can help you calculate a figure specific to your situation.

Final Thoughts

The best SIP to invest now for your retirement is not a secret fund name that nobody else knows about. It is the SIP that matches your age, your risk appetite, your time horizon, and one that you can stay committed to for the next fifteen, twenty or thirty years without stopping during every market dip.

The data from AMFI makes it clear that millions of Indians have already made systematic investing a monthly habit, and starting today, even with a modest amount, puts the power of long term compounding firmly on your side.

Disclaimer: This article is for general educational purposes only and does not constitute personalised investment advice. Mutual fund investments are subject to market risk. Please read all scheme related documents carefully and consult a SEBI registered investment adviser before making any investment decision.

Stay connected with Malhar Investments for the latest investment insights, retirement planning guidance, and proven wealth-building strategies. 📈💰